What is Medicare?

Medicare is the United States government’s health insurance program for people over 65 years old. Individuals have the option to enroll in different parts of the program depending on their needs. Part B is available for a monthly premium. It is considered “medical insurance” because it covers doctor visits, outpatient care, and some preventative services. Those who already receive Social Security benefits are automatically enrolled in Part B when they turn 65. Otherwise, individuals become eligible for Part B and can begin enrolling three months before the month of their 65th birthday. They remain eligible for three months after their birthday month. Enrolling in Part B is not mandatory. However, several factors must be considered during your eligibility period.

How Does Medicare Work?

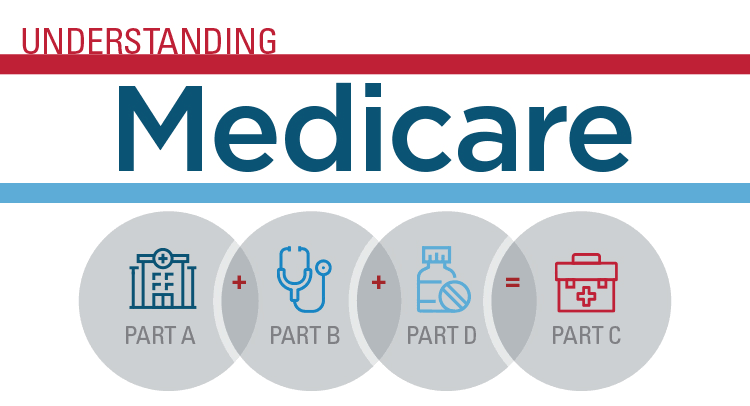

The program is split into four parts. Part A covers hospital services and inpatient treatment. It is free to most Americans who paid Medicare taxes. Part B covers a variety of outpatient healthcare services and is paid for out-of-pocket through a monthly premium. The price is fixed for most Americans. Some high-income individuals may have a higher premium though. Advantage Plans, formerly known as Part C, bundle Part A and B together with dental, vision, and prescription drug coverage. Part D is separate prescription drug coverage.

What Services are Covered by Part B?

Part B splits coverage into two categories, medically necessary services and preventative services. Essentially, Part B covers treatments for illnesses and services that detect diseases. Visits with specialists who manage conditions like neurologic or cardiac conditions and mental health professionals are included in Part B.

It also covers Durable Medical Equipment, like walkers and oxygen supplies, that a doctor prescribes. Although Medicare is a national program, covered services vary by state based on standards set at the federal level, local coverage determinations, and decisions made by billing companies.

Medically necessary services are treatments ordered by a physician to treat, monitor, or diagnose a condition. Examples of services that fall under Part B include:

- Chemotherapy treatment and other prescription drugs administered in a doctor’s office or clinic

- Laboratory Testing or Bloodwork

- CTs, MRIs, and Echocardiograms

- Ambulance Service and ER Visits

- Physical Therapy

Preventative services are tests or evaluations ordered by a doctor to detect disease or protect against future illness. Examples of these services covered by Part B include:

- Diabetes Screening

- Bone Density Testing

- Cancer Screenings like Mammograms and Colorectal Tests

- Tests for Heart Disease

- Flu, Hepatitis, and Pneumonia Vaccinations

The Costs of Part B

The cost of coverage is based on your income. Medicare revises premiums, co-insurance, and deductibles yearly, so the prices are not fixed. The standard premium for Part B coverage in 2021 was $148.50. Part B coverage also carries a deductible. This is the amount you must spend out-of-pocket before the insurance begins covering expenses. The deductible was $203 in 2021. Co-insurance is your responsibility for a covered service once the deductible is met. It is typically 20 percent.

Reasons to Enroll in Part B

Healthy aging depends on preventing disease, detecting medical problems in their early stages, and treating illnesses when they occur. Managing ongoing medical conditions and getting preventative services are important. Consistent treatment limits complications and the progression of diseases. Enrolling in Part B is valuable because it covers many of the services needed to prevent and manage illness. Without coverage, you may be forced to pay out of pocket for necessary treatments or forego screenings that detect things like cancer in their earliest, most treatable stages.

If you decline to enroll in Part B once you become eligible, you’re able to join during the open enrollment periods. However, you will pay a penalty. The premium and deductibles are adjusted each year, but individuals who delay enrolling will pay a higher premium once they do join the program.

Reasons to Decline Part B

Financial and healthcare decisions must be made with all the facts. Each situation is different. Certain individuals may have post-retirement healthcare through their former employer or union. This coverage may be adequate but carefully review your benefits and eligibility. It is best to check with your plan manager to confirm your coverage. Some plans only cover deductibles or coinsurance and act as secondary coverage to Medicare. Declining Part B may benefit you, but a change in private insurance could have a ripple effect.

Part B is redundant if you choose an Advantage or Part C Plan. Because these programs bundle the services from Parts A and B, along with dental and vision care, necessary coverage is secured without separate enrollment in Part B.

Make an Informed Decision

Selecting the correct Medicare coverage is important. Be aware of your eligibility dates and enrollment deadlines, to find out if you are eligible visit ClearmatchMedicare. Missing them can result in financial penalties or gaps in coverage. Medical insurance that covers preventative and medically necessary care is essential for healthy aging. It is critical to make sure you are adequately covered, either through Part B, an Advantage plan, or private insurance.